In a remote village where banks are hours away and mobile phones are more common than electricity, a woman makes a transaction through a simple text. She is not just sending money. She is stepping into the financial system.

That is the power of digital finance in developing economies. It has become more than convenient. It is an opportunity. It is survival. And in many places, it is a revolution.

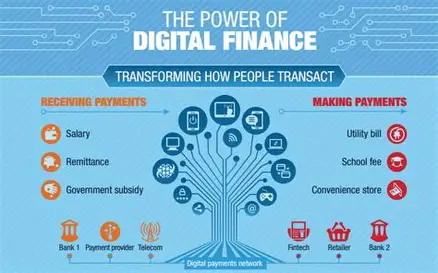

From mobile wallets to blockchain solutions, digital finance is transforming how people in low-income and middle-income countries access, use, and grow their money. But with this transformation comes real challenges. Infrastructure. Trust. Regulation. And digital literacy.

This article uncovers both sides of the story. The wins that are changing lives. And the barriers that must still be overcome.

A quiet revolution. Digital finance is rewriting access where banks cannot reach.

1. What is Digital Finance?

Digital finance refers to the use of digital technologies to provide financial services. It includes mobile payments, online banking, microloans, insurance, peer-to-peer lending, and cryptocurrency platforms.

For developing economies, digital finance is not just about digitizing old systems. It is about creating entirely new systems for populations who were never part of traditional finance in the first place.

It bridges the gap between cash-based cultures and formal economic participation.

One term, many tools. Digital finance includes a full spectrum of services beyond just banking.

2. The Wins: How Digital Finance is Changing Lives

a. Financial Inclusion for the Unbanked

According to the World Bank, over one billion adults worldwide still lack access to traditional banking. But many of these same people now own a mobile phone.

Digital finance turns phones into financial tools. People can:

Send and receive payments

Save securely

Access microloans

Pay bills and school fees

In Kenya, the mobile money platform M Pesa helped lift over one million people out of poverty by giving them access to basic financial services.

b. Empowering Women and Rural Communities

In many societies, women and rural populations are sidelined by traditional banks. Digital wallets let them control their income, start small businesses, and build credit history.

c. Crisis Resilience

During the pandemic, governments used digital payment systems to distribute relief. In Nigeria, India, and Brazil, digital platforms ensured that help reached even the most isolated citizens.

Ownership through access. Digital tools empower small business owners across the world.

3. Real Success Stories

M Pesa in Kenya

Launched in 2007, M Pesa became a model for mobile money success. By allowing users to deposit, withdraw, and transfer money through text messages, it became a game-changer.

Today, more than 90 percent of Kenyan adults use M Pesa, making Kenya one of the most financially connected populations in Africa.

Paytm in India

Starting as a mobile recharge app, Paytm grew into a full-scale digital bank. It helped millions of Indians pay bills, transfer money, and shop digitally, especially in smaller towns.

Wave in West Africa

Wave, a mobile money startup, disrupted the market by slashing transfer fees and offering a user-friendly interface. In Senegal and Côte d’Ivoire, it has become a dominant player.

Local heroes. Mobile finance agents are key to expanding reach and building trust.

4. The Key Drivers Behind Digital Finance Growth

a. Mobile Penetration

Even in rural areas, basic mobile phone ownership is high. This has created a digital bridge for financial services to cross.

b. Urban to Rural Remittances

Digital wallets make it easier for migrant workers to send money back to families without long queues or risky cash travel.

c. Entrepreneurial Innovation

Fintech startups are creating tailored solutions for underserved communities, offering everything from crop insurance to pay-as-you-go solar financing.

d. Government Policies and Partnerships

Public-private partnerships have helped scale digital finance infrastructure. Initiatives like India’s Aadhaar identity system allowed for faster onboarding into digital banking.

Innovation meets infrastructure. Even simple setups can power complex transactions.

5. The Challenges Holding Back Progress

a. Poor Connectivity and Electricity Access

In regions with unreliable internet or power, digital services face real limitations. Without stable networks, adoption suffers.

b. Digital Illiteracy

Having a phone does not mean knowing how to use apps or secure passwords. Many first time users are vulnerable to fraud and misuse.

c. Lack of Regulation

In some countries, digital finance grows faster than laws can follow. This leads to gaps in consumer protection, data privacy, and transaction safety.

d. Gender Gaps and Social Barriers

Women in some regions still face cultural or logistical barriers to owning phones or registering accounts.

e. Overdependence on Mobile Operators

If the digital ecosystem relies on just one or two telcos, any technical failure or price hike can disrupt the whole financial chain.

Opportunity interrupted. Infrastructure gaps still slow down financial access.

6. The Human Element: Trust and Behavior

Technology can only go so far. Real adoption depends on human behavior.

People must:

Trust the system

Understand how it works

Feel safe using it

In some communities, word of mouth and social proof are more powerful than advertisements. That is why successful digital finance platforms often rely on local agents and peer educators.

Knowledge is power. Building trust begins with building understanding.

7. The Future of Digital Finance in Developing Economies

a. Biometric Verification

Fingerprint or facial recognition can simplify onboarding while improving security for users who lack a formal ID.

b. Blockchain for Transparency

Blockchain technology offers secure, traceable transactions. This could revolutionize public welfare payments and prevent corruption.

c. Artificial Intelligence for Micro Credit

AI can help assess credit risk based on mobile usage or transaction history, offering fairer loans to informal workers and small businesses.

d. Offline Payments

New solutions allow people to make transactions without the internet, using Bluetooth or encrypted SMS.

Safer access, smarter systems. The future of finance is not just digital, it is intelligent.

8. Policy Recommendations for Sustainable Growth

For digital finance to grow responsibly in developing economies, collaboration is key. Policymakers, fintech companies, nonprofits, and telecoms must work together.

Recommendations include:

Investing in rural connectivity

Providing digital literacy education in local languages

Creating robust consumer protection frameworks

Encouraging competition to keep fees low

Promoting financial products tailored to local needs

Change through partnership. Policy plays a crucial role in expanding financial inclusion.

Conclusion: A Gateway to Transformation

Digital finance is not a silver bullet. But it is a powerful key. A key that opens doors to inclusion, to security, and to hope.

In developing economies, where traditional banking failed or never arrived, mobile phones and smart systems are stepping in. And as long as we listen, adapt, and build with empathy, this quiet revolution will continue to grow louder.

The future of finance is not just about apps or algorithms. It is about people. And their right to access the tools that help them build a better life.

From invisible to included. Digital finance is transforming lives one transaction at a time.